Don’t let capital gains eat your profits. Learn how a 1031 Exchange allows real estate investors to defer taxes and scale their portfolios indefinitely.

Table of Contents

I’ll never forget a meeting I had with a seasoned investor named David a few years back. He had owned a small, slightly run-down duplex in a neighborhood that had suddenly become the hottest spot in the city. He bought it for $200,000, and it was now worth nearly $800,000. On paper, he was thrilled. But the moment we sat down to talk about selling, his face fell.

“If I sell this,” he told me, “the IRS is going to take a massive chunk of my hard-earned equity. I’ll be left with way less than I need to buy my next property.”

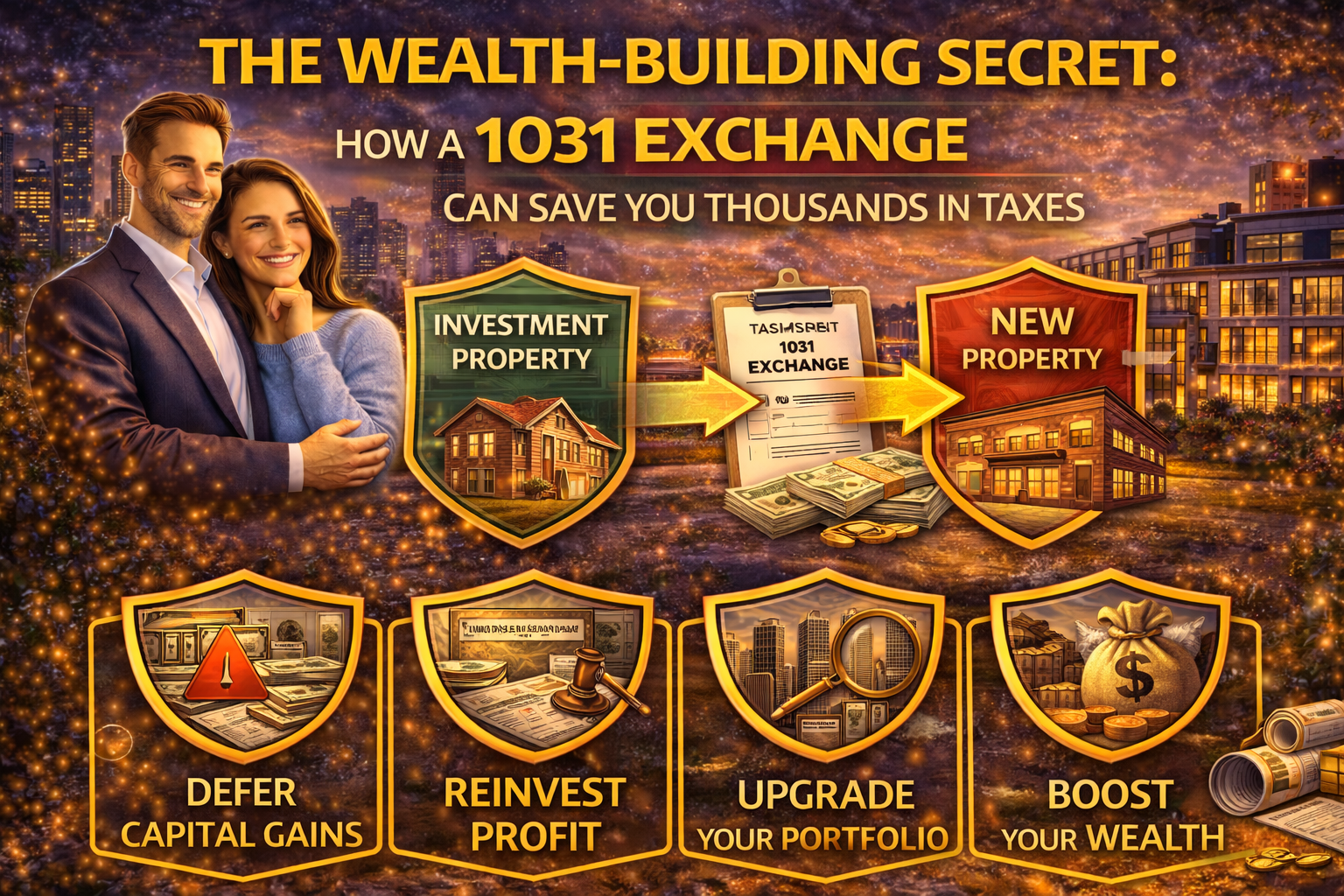

This is the “investor’s trap.” You do everything right—you pick a great location, you manage the property well, and you build significant equity—only to realize that Uncle Sam wants a seat at the closing table. This is exactly where the 1031 Exchange comes in. It is, quite simply, one of the most powerful wealth-building tools ever written into the tax code.

By using a 1031 Exchange, David didn’t have to settle for a smaller replacement property. He was able to reinvest 100% of his proceeds into a larger, more profitable apartment complex, deferring every penny of his capital gains tax. It’s not a tax loophole; it’s a strategic reinvestment bridge that allows you to keep your money working for you rather than sending it off to the treasury.

What Exactly is a 1031 Exchange?

Named after Section 1031 of the Internal Revenue Code, this maneuver allows an investor to sell an investment property and “exchange” it for a new one of “like-kind” while deferring the taxes that would normally be due upon sale. Think of it as a government-sanctioned way to kick the tax can down the road.

The beauty of the 1031 Exchange is that there is no limit to how many times you can do it. You can start with a single-family rental, exchange it for a four-plex, then later move into a retail strip center. You are essentially using the government’s money (the tax you would have paid) as an interest-free loan to scale your real estate portfolio.

The Strict Rules of the Game

While the benefits are massive, the IRS is incredibly picky about how you execute a 1031 Exchange. You can’t just sell a house, put the money in your personal savings account for a month, and then buy another one. If you even touch the money, the “exchange” is broken, and you’ll owe the full tax amount immediately.

1. The 45-Day Identification Window

The clock starts ticking the moment you close the sale of your “relinquished” property. You have exactly 45 days to identify potential replacement properties. This is usually the most stressful part of the process. You must submit a written list of the properties you might buy to your Qualified Intermediary.

2. The 180-Day Closing Deadline

From the day you sell your original property, you have a total of 180 days to officially close on your new “replacement” property. This isn’t 45 days plus 180; it’s 180 days total. If your closing gets delayed on day 181, your 1031 Exchange fails, and the tax bill comes due.

3. The Qualified Intermediary (QI)

To keep the IRS happy, you must use a Qualified Intermediary. This is a third-party entity that holds the proceeds from your sale in a secure account and then transfers those funds directly to the seller of your new property. Again, you must never have “constructive receipt” of the cash.

Why Investors Love the “Like-Kind” Definition

A common misconception is that if you sell a condo, you have to buy another condo. Luckily, that’s not how it works. In the world of the 1031 Exchange, “like-kind” is defined very broadly.

You can sell raw land and buy an industrial warehouse. You can sell a single-family rental and buy a fractional interest in a massive commercial complex. As long as both properties are held for “productive use in a trade or business or for investment,” the IRS considers them like-kind. This flexibility is what allows investors to pivot their strategy as they age or as the market changes.

According to the National Association of Realtors (NAR), the 1031 Exchange is a vital driver of liquidity in the commercial and residential investment markets. Without it, many investors would simply hold onto stagnant properties forever to avoid the tax hit, causing the entire market to slow down.

Understanding “Boot” and How to Avoid It

In a perfect 1031 Exchange, you buy a new property that is equal to or greater in value than the one you sold. You also must carry over the same amount of debt (mortgage) or more.

If you trade down in value, or if you have a smaller mortgage on the new property, that difference is called “boot.” The IRS views boot as a taxable gain. For example, if you sell for $500k but only buy for $450k, that $50k difference is going to be taxed. To maximize the savings of your 1031 Exchange, you generally want to “reinvest all” to ensure zero boot is created.

Scaling Up: The Power of Compound Growth

Let’s look at the math, because it’s staggering. Imagine you have $100,000 in capital gains. If you don’t use a 1031 Exchange, and you’re in a 20% tax bracket (plus state taxes and depreciation recapture), you might lose $30,000 of that immediately.

That $30,000 could have been the down payment on an additional $120,000 worth of real estate. Over 20 years, that extra property could grow into hundreds of thousands of dollars in equity. By using a 1031 Exchange every time you sell, you are essentially compounding your wealth at a much higher rate because you are investing with the full power of your gross proceeds, not your “after-tax” crumbs.

For those interested in the deep legal history of this code, Wikipedia’s entry on Internal Revenue Code Section 1031 offers a fascinating look at how these rules have survived various tax reforms over the last century. It’s a testament to how much the government values real estate investment as a pillar of the economy.

The “Swap ‘Til You Drop” Strategy

This is the ultimate long-term play for real estate families. You can use a 1031 Exchange throughout your entire life, moving from property to property, building a massive empire of rentals.

If you hold those properties until the day you pass away, your heirs receive a “stepped-up basis.” This means the capital gains tax you’ve been deferring for decades simply vanishes. Your children inherit the property at its current market value, and all that deferred tax from every 1031 Exchange you ever did is essentially forgiven. It is the single most effective way to transfer generational wealth.

FAQ Section

Can I use a 1031 Exchange for my primary residence? No. This strategy is strictly for investment or business properties. If you live in the house, you’ll likely want to look into the Section 121 exclusion, which allows individuals to exclude up to $250,000 of gain (or $500,000 for couples) from the sale of a primary home.

What happens if I can’t find a replacement property in 45 days? If the 45-day window closes and you haven’t identified a property in writing through your QI, the 1031 Exchange is cancelled. The intermediary will release the funds to you, and you will be responsible for paying the capital gains tax on your next tax return.

Is there a minimum holding period for the property? The IRS doesn’t specify a “perfect” number, but most tax professionals recommend holding a property for at least one to two years to prove it was an investment and not a “flip.” “Flipping” houses is considered a business activity, not an investment, and does not qualify for a 1031 Exchange.

Can I do a “Reverse” 1031 Exchange? Yes, but it’s more complex and expensive. A reverse 1031 Exchange happens when you find the perfect new property and want to buy it before you’ve sold your current one. You still need an intermediary to hold the title of one of the properties during the process.

Do I have to buy the replacement property in the same state? Usually, yes, within the United States. You can sell a rental in Florida and buy a warehouse in Texas using a 1031 Exchange. However, you cannot generally exchange domestic property for international property.

Conclusion

At the end of the day, real estate investing is about maximizing your “return on equity.” If a huge chunk of your equity is being siphoned off by taxes every time you want to upgrade your portfolio, you’re playing the game with one hand tied behind your back.

The 1031 Exchange is your way to stay in the game at full strength. It requires careful planning, a great Qualified Intermediary, and a tight eye on the calendar, but the financial rewards are truly life-changing. If you’ve built up significant value in a property and are thinking about your next move, don’t let the tax bill scare you—let a 1031 Exchange empower you to reach that next level of wealth.